The Global Count-Down To Financial Devastation iN 2018 As Told By The Economist, And The Rationale Behind The New World Currency

The Global Count-Down To Financial Devastation In 2018 As Told By The Economist, And The Rationale Behind The New World Currency

SHORT COMMENTARY BY MATTHIAS CHANG:

I HAVE ANALYSED CYCLES IN ALL MY

PUBLICATIONS AND ARTICLES. THESE CYCLES ARE NOT COINCIDENCES. AND I HAVE

DISCLOSED IN MY LATEST BOOK, “THE QI OF LONGEVITY – HOW TO SURVIVE IN

TIMES OF VOLATILITY” HOW TO USE A SPECIAL METHOD (BASED ON THE ANCIENT

CHINESE SYSTEM OF “QIQONG” AND “I CHING” TO APPRECIATE THE ACCURACY AND

THE CONSEQUENCES OF SUCH CYCLES. ALREADY, THERE ARE SOME DEVIOUS

AR*&%^## WHO ARE PLAGIARISING MY RESEARCH AND CLAIMING THAT THIS

METHOD IS THEIR DISCOVERY. THEY ARE FAKE CON ARTISTS, INDULGING IN

INTELLECTUAL MASTURBATION BECAUSE THEY DO NOT KNOW ANYTHING ABOUT

QIQONG AND OR I CHING. PLEASE READ THE BELOW REVELATION AND GET

PREPARED!

THE COUNT-DOWN

1988 * 1998 * 2008 * 2018

THE TEN YEARS CYCLE

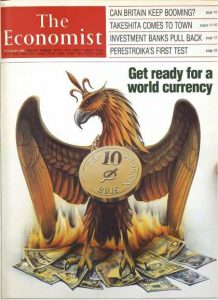

LOOK AT THE DATE STAMPED ON THE “COIN” 2018!

The Economist – January 9, 1988, Vol. 306, pp 9-10

THIRTY years from now,

Americans, Japanese, Europeans, and people in many other rich countries,

and some relatively poor ones will probably be paying for their

shopping with the same currency. Prices will be quoted not in dollars,

yen or D-marks but in, let’s say, the phoenix. The phoenix will be

favoured by companies and shoppers because it will be more convenient

than today’s national currencies, which by then will seem a quaint cause

of much disruption to economic life in the last twentieth century.

At the beginning of 1988 this appears an

outlandish prediction. Proposals for eventual monetary union

proliferated five and ten years ago, but they hardly envisaged the

setbacks of 1987. The governments of the big economies tried to move an

inch or two towards a more managed system of exchange rates – a logical

preliminary, it might seem, to radical monetary reform. For lack of

co-operation in their underlying economic policies they bungled it

horribly, and provoked the rise in interest rates that brought on the stock market crash of October. These events have chastened exchange-rate reformers. The

market crash taught them that the pretence of policy co-operation can

be worse than nothing, and that until real co-operation is feasible

(i.e., until governments surrender some economic sovereignty) further

attempts to peg currencies will flounder.

But in spite of all the trouble

governments have in reaching and (harder still) sticking to

international agreements about macroeconomic policy, the conviction is

growing that exchange rates cannot be lef to themselves. Remember that

the Louvre accord and its predecessor, the Plaza agreement of September

1985, were emergency measures to deal with a crisis of currency

instability. Between 1983 and 1985 the dollar rose by 34% against the

currencies of America’s trading partners; since then it has fallen by

42%. Such changes have skewed the patern of international comparative

advantage more drastically in four years than underlying economic forces

might do in a whole generation.

In the past few days the world’s main

central banks, fearing another dollar collapse, have again jointly

intervened in the currency markets. Market- loving ministers such as

Britain’s Mr. Nigel Lawson have been converted to the cause of

exchange-rate stability. Japanese ofcials take seriously he idea of

EMS-like schemes for the main industrial economies. Regardless of the

Louvre’s embarrassing failure, the conviction remains that something

must be done about exchange rates.

Something will be, almost certainly in

the course of 1988. And not long after the next currency agreement is

signed it will go the same way as the last one. It will collapse.

Governments are far from ready to subordinate their domestic objectives

to the goal of international stability. Several more big exchange-rate

upsets, a few more stock market

crashes and probably a slump or two will be needed before politicians

are willing to face squarely up to that choice. This points to a muddled

sequence of emergency followed by a patch-up followed by emergency,

stretching out far beyond 2018 – except for two things. As time passes,

the damage caused by currency instability is gradually going to mount;

and the very tends that will make it mount are making the utopia of

monetary union feasible.

The new world economy

The biggest change in the world

economy since the early 1970’s is that flows of money have replaced

trade in goods as the force that drives exchange rates as a

result of the relentless integration of the world’s financial markets,

differences in national economic policies can disturb interest rates

(or expectations of future interest rates) only slightly, yet still

call forth huge transfers of financial assets from one country to

another. These transfers swamp the flow of trade revenues in their

effect on the demand and supply for different currencies, and hence in

their effect on exchange rates. As telecommunications technology

continues to advance, these transactions will be cheaper and faster

still. With unco-ordinated economic policies, currencies can get only

more volatile.

In all these ways national economic boundaries are slowly dissolving.

As the trend continues, the appeal of a currency union across at least

the main industrial countries will seem irresistible to everybody except

foreign-exchange traders and governments. In the phoenix zone, economic

adjustment to shifts in relative prices would happen smoothly and

automatically, rather as it does today between different regions within

large economies (a brief on pages 74-75 explains how.) The absence of

all currency risk would spur trade, investment and employment.

The phoenix zone would impose

tight constraints on national governments. There would be no such thing,

for instance, as a national monetary policy. The world phoenix supply would be fixed by a new central bank ,

descended perhaps from the IMF. The world inflation rate – and hence,

within narrow margins, each national inflation rate- would be in its

charge. Each country could use taxes and public spending to offset

temporary falls in demand, but it would have to borrow rather than print

money to

finance its budget deficit. With no recourse to the inflation tax,

governments and their creditors would be forced to judge their borrowing

and lending plans more carefully than they do today. This means a big

loss of economic sovereignty, but the trends that make the phoenix so

appealing are taking that sovereignty away in any case. Even in a world

of more-or-less floating exchange rates, individual governments have

seen their policy independence checked by an unfriendly outside world.

As the next century approaches,

the natural forces that are pushing the world towards economic

integration will offer governments a broad choice. They can go with the

flow, or they can build barricades. Preparing the way for the

phoenix will mean fewer pretended agreements on policy and more real

ones. It will mean allowing and then actively promoting the

private-sector use of an international money alongside existing national

monies. That would let people vote with their wallets for the eventual

move to full currency union. The phoenix would probably start as a

cocktail of national currencies, just as the Special Drawing Right is

today. In time, though, its value against national currencies would

cease to matter, because people would choose it for its convenience and

the stability of its purchasing power.

The alternative – to preserve

policymaking autonomy- would involve a new proliferation of truly

draconian controls on trade and capital flows. This course

offers governments a splendid time. They could manage exchange-rate

movements, deploy monetary and fiscal policy without inhibition, and

tackle the resulting bursts of inflation with prices and incomes

polices. It is a growth-crippling prospect. Pencil in the phoenix for around 2018, and welcome it when it comes.

The Economist -September 24, 1998

One world, one money

A global currency is not a new idea, but it may soon get a new lease of life

IN DIFFICULT times, people are allowed,

even encouraged, to think the unthinkable. Some of the economists who

propose capital controls as a remedy for recession in Asia claim to be

doing this—but they are flattering themselves. Unthinkable? Malaysia

just did it. Dozens of countries still use capital-account restrictions.

And it is a cliché of the orthodox “sequencing” literature that a

variety of such controls should be retained until other reforms are

complete. Really, to think the unthinkable, you have to be bolder than

this.

So here is an idea: global currency

union. Let nobody call it boringly feasible, or politically expedient.

Yet, like all the best unthinkable ideas, it has more going for it than

you might think—in principle, at least. The idea is not new. Richard

Cooper of Harvard University proposed a single world currency in Foreign Affairs

in 1984, and he was not the first to think of it. It seemed an

outlandish idea, and still does. But much has happened lately to make it

worth a moment’s thought.

The usual way to ask whether countries

would be better off sharing a single currency—that is, whether they

constitute an “optimal currency area”—is to examine the following

trade-off. On one side is the undoubted convenience of a single money as

a lubricant for trade and cross-border investment. On the other is the

loss of the exchange rate as a shock-absorber for times when one or more

of the countries face pressures (an abrupt fall in demand for their

exports, say, or a sudden rise in labour costs) that the others are

spared—a so-called “asymmetric shock”.

In setting cost against benefit, again

according to the standard view, the crucial factors are openness to

trade and freedom of movement of factors of production. A small open

economy has more to gain from the convenience provided by a single

currency. On the other hand, if labour (especially) is reluctant to

migrate, the need for the exchange-rate shock-absorber is all the

greater. Weighing all this, most economists conclude that the 11

countries that are about to adopt the euro are not in fact an optimal

currency area. The world as a whole is not even close.

So what has changed? The main thing is

the current global emergency. This is so serious a crisis that it is

likely to prove a paradigm-shifting event, though straws were in the

wind already. The emerging-market disaster poses the question, How is

the world to live with globally integrated finance? In addition, it

casts doubt on what once seemed a good answer: that floating exchange

rates are the best way to stabilise the world economy.

Shockingly unstable

According to the traditional model, a

country with unduly high labour costs, and therefore a troublesome

current-account deficit, could expect to see its currency depreciate;

this would cut real wages, making imports dearer and exports cheaper,

thus neatly restoring the economy to equilibrium. But in a world where

international flows of capital overwhelm international flows of trade,

this does not work. Floating exchange rates destabilise trade and

investment by wrenching relative prices away from their fundamental

values (that is, from the values that would put the corresponding

exchange rates at purchasing-power parity). In the emerging-markets

crisis that currently threatens the world economy, exchange-rate

movements have not been absorbers of shocks but amplifiers and even

creators of them.

Governments of small open economies have

long known that it is not an option to “leave the exchange rate to the

market”. Monetary policy must always keep at least one eye on the

currency. But governments have also learnt, in a second big change, that

intermediate exchange-rate regimes do not work either. That was the

lesson of the European Monetary System debacle of 1992-93 (and,

arguably, of the downfall of the pegged-but-adjustable regimes used in

Asia until last year). Semi-fixed systems cannot withstand the assault

of integrated capital markets: they are prone to self-fulfilling panics.

In other words, they too are destabilising.

But what does that leave? Let’s see.

Pure floating is no use. Semi-fixed is no use. So there are two

possibilities. One is to turn back the clock on financial integration:

then pure-floating or semi-fixed systems might once again be used

successfully. That would be enormously costly, especially to the

developing countries; and it would be very difficult, because

integration is partly driven by technological progress, which is hard to

reverse. Still, it is a fair bet that a lot of countries will follow

Malaysia’s example and give it a try. Otherwise, it seems, the remaining

course is to combine increasing integration with perfect fixity of

exchange rates—meaning currency union.

The fashion for currency boards reflects

some of this thinking. Exchange-rate flexibility is more trouble than

it is worth, advocates say, so abandon it once and for all. Alas,

currency boards suffer big drawbacks all of their own. Whereas a

currency union has a central bank to act as lender of last resort, a

country with a currency board does not. So these regimes are vulnerable

to runs on banks. Currency boards are a poor test of the larger idea.

The all-or-nothing, float-or-merge

analysis also provides the case in economic logic for the euro: strive

for integration, it says, no holds barred. Unfortunately, EMU is a

somewhat flawed test as well. It is a political project as much as an

economic one, so it will not reveal everything about how well a currency

union among independent nation states might work. But it will reveal a

lot, and its symbolic importance will be immense. If it fails, not only

will that cause enormous political harm to the European Union, but the

pressure for global financial barriers will be greatly strengthened. If

it succeeds, the case for a global currency union will seem much more

interesting.

Fine, you say, but how

would the world ever get from here to there? Hard to say, admittedly.

Find the answer to that and the idea would be thinkable.

>>http://futurefastforward.com/2017/12/20/global-count-financial-devastation-2018-told-economist-rationale-behind-new-world-currency/<<

>>http://futurefastforward.com/2017/12/20/global-count-financial-devastation-2018-told-economist-rationale-behind-new-world-currency/<<

No comments:

Post a Comment